Those poor millionaires, being asked to contribute to society. How could you?!

Hey. These hard working millionaires are tricking this money down by buying stocks and investing in real estate and then upping the price of rent to continue to increase their wealth so they can push to the next tier of millionaire".

Which they’ve hired accountants to do for them. But I assure you, their work lunches are exhausting

Reposting from another thread:

Social security has been 10-15 years away from being insolvent for 80 years. It will always be 10-15 years away from being insolvent because of the way it’s calculated.

When the CBO or whoever scores it they can predict certain things like the number of recipients, the size of their payments, and inflation. They aren’t allowed to take into account things that Congress may (but definitely will) do in the future, like raising the cap on social security taxes roughly with inflation. It went up from $160200 in 2023 to $168600 in 2024. This is a rare bipartisan, uncontroversial thing. Congress almost always follows the SSA recommendation exactly.

It would be more accurate to say “if the social security cap stays at $168600 for 10 years, social security will be insolvent.”

The people pushing this bullshit know it’s bullshit. They do it to make people think they’ll never get social security so they can get enough voters on board with killing it, like they’ve been trying to do for 88 years.

Don’t fall for it.

That’s populism, and left populism is pretty strong here.

They spend more as they get in, it will run out. No amount of tomfoolery will change that.

They’ve been saying that my entire life, my dad’s entire life, and when my dad was my age, my grandfather would tell him he’s heard the same things his entire life going back to the 40s.

For a couple decades the disingenuous doom -and-gloomers told us no way could social security ever deal with the baby boomers. All through the 80s and 90s they told us we might as well privatize it or kill it all together. The only time wall street shut up about it was when they were too busy jerking off to the thought of getting their hands on that money. Well, the youngest of the boomers turn 60 in '24, they’re almost all in and the end times keep getting pushed back, from the 80s to the 90s to the 00s to the 10s to the 20s and now 2035. It’s like a doomsday cult that keeps pushing the date when the apocalypse doesn’t arrive at the appointed time.

You’ll have to excuse me for not getting worked up over the 40th new year I’ve heard for the sky falling.

And for what it’s worth, managing the COLAs, the cap, the percentages, and anything else the SSA has done throughout it’s existence isn’t “tomfoolery,” it’s accounting. And damn good accounting so far. The SSA being such a well run government institution probably makes republicans hate them almost as much as the tax itself.

It is not going to “run out”. That is republican talking point and propaganda. God damn that myth is believed by everyone.

The concepts of solvency, sustainability, and budget impact are common in discussions of Social Security, but are not well understood. Currently, the Social Security Board of Trustees projects program cost to rise by 2035 so that taxes will be enough to pay for only 75 percent of scheduled benefits. ^1

75% of benefits will still be paid in even the worse case scenario. The fear mongering is not necessary.

Vote. Every. Time.

Voting prevents things from getting worse, it doesn’t make things better.

Not sure I agree. Obamacare is better than then nothing-burger that was available before if you didn’t get healthcare through an employer. Biden is trying to at least get some student loan relief through congress. Getting the right people elected to state governments can help make abortions available again in some states. (If you’re a right-wing person then choose the opposite topics for your examples.)

People who are defeatist about voting come across as complainers who are too lazy to get off their butts to help.

While I don’t disagree, the individual mandate was a crucial part of making it work, and also the weakest part of it. There shouldn’t have been an individual mandate without a much larger medicaid supplement or Medicare-for-All as options. A handslap fee for not having insurance was both a worthless penalty and legally shaky from the get-go.

There should’ve been caps on premium and deductible increases that were way more realistic, too. Like rent-control and tied to either a maximum percent of net profit increase, or inflation, etc.

Ultimately I don’t think Obamacare went far enough, and I don’t think there’s an argument to the contrary that’s not in favor of protecting the true enemies of sustainable healthcare, the insurance companies.

Stop spreading this BS. SS going bankrupt is misinformation.

So just to translate for non Americans: Social Security is a kind of guaranteed old age / retirement pension, by the looks of it.

Yea. 6.2% of each paycheck is taken out for SS and your employer will match it. Then, when you turn 67, you are of retirement age and will start reciecving monthly checks proportional to your income when you were working. There are exceptions but that’s generally how it goes

Fucking lazy-ass boomers getting my money.

Lazy-ass boomers that paid into SS their entire lives? Those lazy-ass boomers?

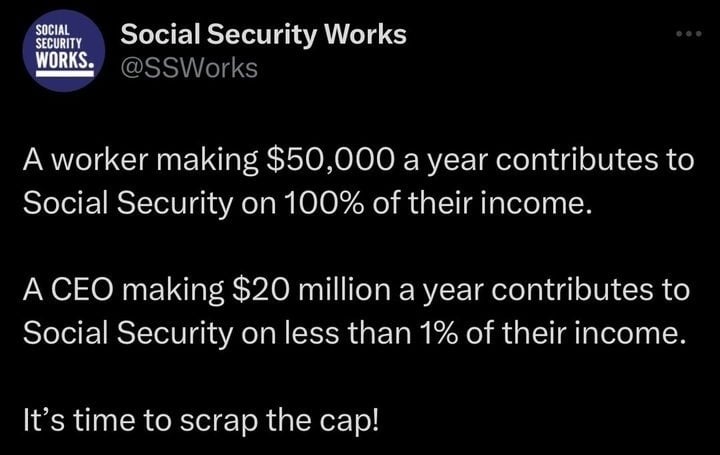

$168,600

That’s the cap. It is clearly and obviously only benefiting the rich. Absolutely insane.

It also benefits the upper middle class. And middle class in HCOL areas.

It should be adjusted based on cost of living.

Making $150k in NYC is like making $50k in middle america.

I literally do not care about the upper middle class.

{kind=link}